In the dynamic world of business, opportunities and challenges often arise unexpectedly. Whether you’re a business owner looking to expand, acquire new assets, or meet immediate cash flow needs, having access to short-term financing can make all the difference. One such financial tool that many businesses use is the bridge loan. This temporary, short-term funding option is designed to help business owners bridge the gap between immediate financial needs and long-term financing solutions.

In this article, we will explore a detailed bridge loan example to illustrate how this type of loan works in a business context, its benefits, and how it can be effectively used to manage short-term financing requirements.

Key Takeaways

Bridge loans provide quick, short-term financing to help businesses manage immediate capital needs.

They are often used for property purchases, acquisitions, working capital, and other time-sensitive opportunities.

Bridge loans come with higher interest rates and require collateral but offer flexibility and rapid access to funds.

Understanding the terms and potential risks is critical for business owners considering bridge loans.

Properly using a bridge loan can enable business owners to move forward with plans while securing longer-term financing solutions.

What is a Bridge Loan?

Before diving into the specific example, let’s first define what a bridge loan is.

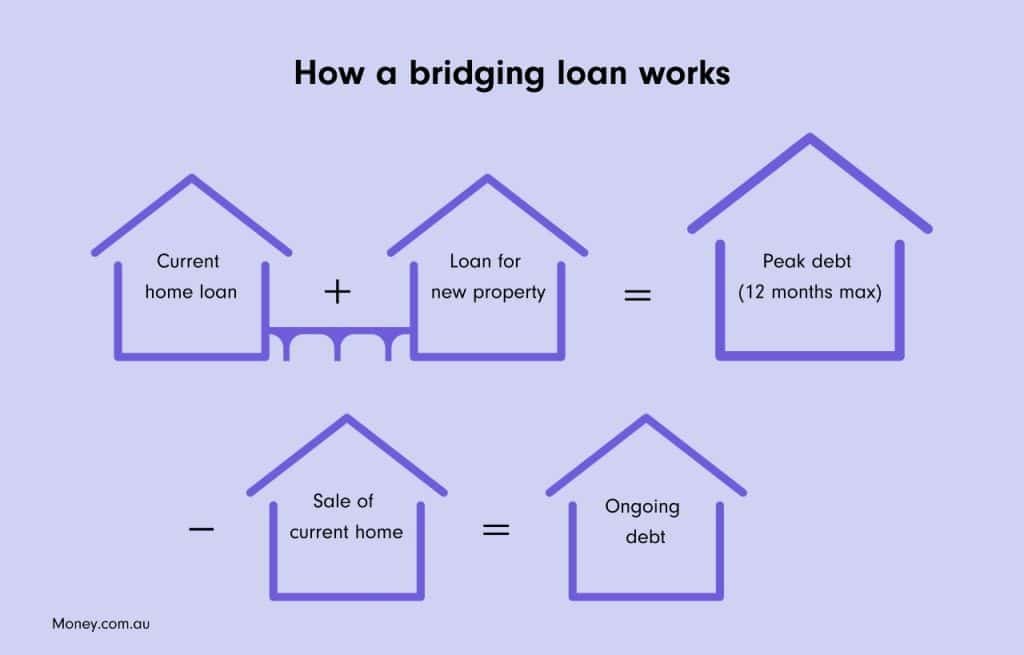

A bridge loan is a short-term loan that helps businesses (and individuals) cover the gap between immediate cash flow needs and a longer-term funding solution. In the business world, it is often used to secure funding quickly for acquisitions, property purchases, or operational expenses when long-term financing is not immediately available.

For example, a business may need to purchase equipment urgently but is waiting for a long-term business loan to come through. A bridge loan can provide the required funds in the short term, with repayment expected once the permanent financing is secured.

Bridge loans are typically secured loans, meaning they are backed by collateral, such as real estate, inventory, or equipment. Because of the short-term nature and the higher risk involved, bridge loans tend to have higher interest rates than traditional loans. However, they are an ideal solution when businesses require immediate capital to take advantage of opportunities or manage cash flow.

A bridge loan is a short-term financing option that is used to cover a temporary cash shortfall while waiting for a long-term financing solution to be secured. Essentially, it “bridges the gap” between immediate financial needs and the availability of more permanent financing. These loans are often used in real estate transactions, business acquisitions, or for covering short-term cash flow needs in a business.

Here’s how a bridge loan works:

Short-Term Financing: Bridge loans are designed to provide funds quickly for a short period, typically between a few months and a year. They are used to address immediate financial needs until a more permanent source of funding, like a traditional business loan, mortgage, or sale of an asset, is available.

Secured Loans: Bridge loans are typically secured by assets, such as real estate, inventory, or equipment, which act as collateral for the loan. If the borrower is unable to repay the loan, the lender can seize the collateral to recover the funds.

Higher Interest Rates: Since bridge loans are short-term and considered higher risk, they tend to have higher interest rates compared to long-term loans. This compensates the lender for the increased risk.

Usage: Businesses and individuals may use bridge loans in several scenarios. Common examples include purchasing a new property before selling an existing one, acquiring a business while waiting for long-term financing, or covering operational costs while awaiting expected payments from clients or customers.

Repayment: Bridge loans are typically repaid in a lump sum or through the proceeds from the longer-term financing once it is secured. The term of repayment can vary, but it is generally designed to align with the timing of the borrower’s larger funding source.

Bridge Loan Example: A Business Scenario

Let’s dive into a real-world business scenario to better understand how a bridge loan can work in practice. Imagine a growing business, “GreenTech Innovations”, which specializes in the development and sale of sustainable technology products.

Business Background:

GreenTech Innovations is a mid-sized company that has recently developed a highly anticipated eco-friendly product. The product has generated a lot of interest in the market, and they are receiving large orders from customers. The business has been profitable, but due to its rapid growth, it has been facing some cash flow challenges, particularly in managing inventory and fulfilling orders.

The company is also in the process of negotiating a long-term loan with a bank that will provide capital for future expansion and inventory procurement. However, the bank’s approval process is taking longer than expected, and GreenTech Innovations needs capital immediately to take advantage of the upcoming orders.

Scenario:

Imagine a small business, “TechToys,” that specializes in selling high-tech gadgets and toys. They have recently identified an opportunity to purchase a batch of cutting-edge products at a discount from a supplier. However, TechToys doesn’t have the cash on hand to make the purchase immediately because they are waiting for approval on a business loan they applied for. If they don’t act quickly, the opportunity will pass them by, and they may lose the chance to secure the discounted products.

To bridge the gap, TechToys applies for a bridge loan from a local lender. The loan amount is enough to cover the cost of purchasing the products, and the loan term is set for six months—just long enough for the business to receive its long-term financing or the funds it expects from a pending sale.

In this example, the bridge loan enables TechToys to secure the opportunity without delay. The business can use the products to boost its inventory, meet customer demand, and generate additional sales. Once the long-term loan is approved, the bridge loan will be repaid.

GreenTech Innovations has received an urgent order worth $200,000 from a large retailer. To fulfill this order, the company needs to purchase materials and hire additional workers for production. The challenge is that the business doesn’t have enough available cash to cover the upfront costs. The long-term loan it’s waiting for has not yet been approved, and the business doesn’t want to miss out on this lucrative opportunity.

Solution: Bridge Loan

GreenTech Innovations decides to apply for a bridge loan to cover the immediate costs of fulfilling the order. They approach a local bank that specializes in short-term business financing.

Bridge Loan Details:

Loan Amount: $200,000

Interest Rate: 10% (higher than a traditional loan due to the short-term and higher risk nature of the loan)

Loan Term: 6 months

Collateral: The company offers its inventory and upcoming payments from customers as collateral.

Purpose: To purchase raw materials, cover labor costs, and fulfill the order while awaiting the approval of the long-term loan.

How the Bridge Loan Works:

The bridge loan is approved quickly, and the funds are made available to GreenTech Innovations within a few days. The business uses the loan to buy the materials, pay workers, and get the order ready for delivery to the retailer. The loan covers the entire $200,000 needed to fulfill the order.

During the next few months, GreenTech continues to work on fulfilling other orders, and the retailer’s payment is expected to come through soon. At the same time, the business’s long-term loan gets approved, providing the funds for continued growth and operations.

Once the long-term loan is finalized and the business receives the funds from the sale of the eco-friendly products, GreenTech Innovations uses the proceeds to repay the bridge loan in full, including the interest. The long-term loan now provides them with the financial stability to continue business expansion and fulfill future orders without relying on short-term financing.

Key Points in the Example:

Quick Access to Funds: The bridge loan allowed GreenTech Innovations to quickly secure the $200,000 needed to fulfill the order. Without the loan, they may have had to turn down the opportunity, which could have damaged their reputation with the retailer and potentially lost out on future business.

Secured by Assets: The loan was secured by inventory and expected payments from customers, which minimized the lender’s risk and made it possible for GreenTech to access the funds even though they were awaiting longer-term financing.

Short-Term Nature: The loan term of 6 months was ideal, giving GreenTech enough time to fulfill the order, receive payments, and repay the loan once their long-term loan came through.

Higher Costs: While the bridge loan was helpful in providing immediate financing, the higher interest rate of 10% reflects the cost of borrowing for short-term needs. However, the cost of the loan was outweighed by the ability to capture the opportunity, complete the order, and generate revenue.

Flexible Use: The bridge loan was used for working capital purposes—primarily to cover the costs of materials and labor. It allowed the business to meet immediate financial obligations while securing long-term financing.

Lessons from the Bridge Loan Example:

Utilizing Bridge Loans for Business Growth: Bridge loans are a powerful tool when businesses need to act quickly to seize an opportunity. In this example, GreenTech Innovations was able to fulfill a large order and position itself for future growth by leveraging bridge financing.

Timing Is Key: While bridge loans offer quick access to capital, it’s crucial that businesses use them for short-term needs that can be addressed within the loan term. In this case, the bridge loan was repaid in a timely manner once the long-term loan was secured.

Plan for Repayment: Businesses should have a clear repayment strategy in place when using bridge loans. GreenTech Innovations was able to repay the loan quickly because it had strong cash flow and anticipated payment receipts.

Risk Management: Bridge loans carry higher interest rates, so businesses should assess whether the short-term financing costs align with the potential benefits of securing the opportunity.

How to Use a Bridge Loan for Business

A bridge loan can be used in various scenarios depending on a business’s needs. Here are several common ways in which businesses can use a bridge loan:

Financing Business Expansion

Business owners often face situations where they need immediate capital to finance expansion plans. This could include purchasing new property, expanding production capabilities, or investing in new technology. A bridge loan can provide the necessary funds to complete these transactions while waiting for long-term financing to be finalized.

Example: A retail business needs additional funds to open a new store in a prime location. They apply for a bridge loan to secure the lease and renovation costs. Once the new store is operational and generating revenue, the business can repay the bridge loan with the profits.

Property Acquisitions and Real Estate Deals

Bridge loans are commonly used in real estate transactions, especially for property purchases. If a business is buying a new property but needs to close the deal before it can access long-term financing, a bridge loan can provide the capital required for the down payment or full purchase price.

Example: A restaurant owner wants to purchase a new commercial property but needs quick access to funds. A bridge loan helps them secure the property while they wait for their traditional commercial loan to be approved.

Mergers and Acquisitions

In cases where a business is acquiring another company or merging with another business, a bridge loan can help finance the deal in the short term. It ensures that the acquisition process moves forward without delays, particularly when the business is waiting for longer-term funding to come through.

Example: A tech startup is in the process of acquiring a smaller competitor. The startup has applied for a larger acquisition loan but needs immediate funds to complete the purchase. A bridge loan is used to cover the acquisition cost, with the loan repaid once the larger loan is finalized.

Working Capital Needs

Bridge loans can also be used for short-term working capital needs, such as covering payroll, purchasing inventory, or addressing cash flow gaps. When a business is waiting for accounts receivable payments to come in or other sources of income, a bridge loan can ensure smooth operations without disruption.

Example: A small manufacturing business has a large order to fulfill but is waiting for payments from previous clients. A bridge loan covers the costs of purchasing raw materials and paying workers until the expected payments arrive.

Pros and Cons of Using a Bridge Loan

Before applying for a bridge loan, it’s important for business owners to understand the pros and cons of using this type of financing.

Pros:

Quick Access to Funds: The most significant advantage of a bridge loan is its speed. Businesses can get the funds they need quickly, often within a few days, to take advantage of immediate opportunities.

Flexible Use: A bridge loan can be used for various purposes, including business expansion, property purchases, or addressing temporary cash flow gaps.

Helps Bridge the Gap: It allows businesses to proceed with plans and opportunities while waiting for longer-term funding or the sale of assets.

Short-Term Financing: Because bridge loans are short-term, businesses don’t commit to long-term debt and can repay the loan quickly once their long-term funding is secured.

Cons:

Higher Interest Rates: Bridge loans generally have higher interest rates than traditional loans, reflecting the higher risk involved.

Short-Term Debt: While a bridge loan is ideal for short-term needs, it may create pressure to repay the loan quickly once the term is up.

Collateral Requirements: Many bridge loans require collateral, which could put the business’s assets at risk.

Fees and Penalties: Bridge loans may come with additional fees, such as origination fees or prepayment penalties.

Also Read : Quick And Easy Short Term Loans: Fast Financing For Urgent Needs

Conclusion

A bridge loan is an invaluable tool for business owners who need quick access to funds to bridge the gap between immediate financial needs and long-term solutions. Whether for expansion, property acquisition, or managing cash flow, bridge loans provide the flexibility and speed necessary to keep a business moving forward.

However, business owners must carefully consider the terms, interest rates, and risks involved with bridge loans. While they offer immediate solutions, they also come with short-term debt obligations and higher costs than traditional loans.

In conclusion, bridge loans are a practical financial tool for businesses, but like any form of financing, they must be used wisely. If managed properly, bridge loans can fuel business growth, help seize timely opportunities, and ensure smooth operations until more permanent financing is secured.

FAQs

What is a bridge loan used for in business? A bridge loan is typically used to meet short-term financial needs, such as purchasing inventory, acquiring real estate, or financing an acquisition, while waiting for longer-term funding or cash flow.

How long is the term of a bridge loan? Bridge loans are usually short-term, typically ranging from a few months to one year, depending on the business’s needs and the lender’s terms.

What is the interest rate on a bridge loan? Interest rates for bridge loans are generally higher than traditional loans due to the short-term and higher-risk nature of the loan. Rates can vary based on the lender and the business’s creditworthiness.

Do I need collateral for a bridge loan? Most bridge loans are secured, meaning the borrower must offer collateral, such as property, inventory, or equipment, to secure the loan.

Can I apply for a bridge loan if I have poor credit? While credit score is a factor, bridge loans are often approved based on the collateral and the business’s ability to repay the loan. If you have valuable assets, you may still qualify.

How do I repay a bridge loan? Bridge loans are typically repaid in a lump sum, either when long-term financing is secured or when the anticipated cash flow becomes available.

Are there any risks associated with bridge loans? Yes, bridge loans come with risks such as high interest rates, the need for collateral, and the potential for pressure to repay the loan quickly. It’s essential to ensure that long-term financing will be available to repay the loan.